We just held our annual webinar on the state of the European FoodTech ecosystem (we’ll have another one in French in two weeks, you can register here). First, I would like to thank all the participants. You can access the video of the webinar here.

This webinar has been the opportunity to answer many questions and to think about the future of the ecosystem. Indeed, the context has dramatically changed since the start of the year.

First, the negative side:

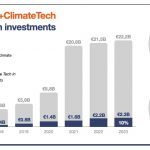

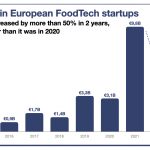

- We observe a diminution in the amounts invested globally in FoodTech startups. It is not that fewer deals are made; it is mostly that large deals (€100M+) are less frequent. There is somehow a flight to quality (i.e., the startups that have a strong path to profitability or have the ability to “sell a huge vision”). Basically, investors still have their pockets full of cash, but as they feel that it will be harder to replenish them (due to the financial tightening underway), they are less keen to make bold bets and focus on their portfolios. So if you have already deep-pocketed investors on board, everything is ok. If not, you better be a startup with a strong model.

- Doubts are rising in some categories of the ecosystem (notably plant-based foods and quick-commerce).

However, we are overall positive with more reasons to see the glass as half full than half empty:

- The situation that I just described doesn’t affect yet (let’s cross fingers) early-stage deals (startups that are emerging and raising little amounts of money to prove their technology or model). Hence, the “future” is preserved as more and more deals are made in all the categories of the ecosystem (notably in startups betting on bold solutions).

- The appetite for FoodTech is still growing (the number of readers of this newsletter and participants in our webinars is a basic but efficient proof of that).

- We have even more reasons for optimism in Europe. The appetite from investors and food corporations for European startups is stronger than ever (notably from Asian companies, something quite new). Even more, well-known bottlenecks (such as the limited number of spinoffs coming out of European universities) are easing.

In a word, we believe in a scenario of a “soft landing” for the FoodTech ecosystem in 2022 in which we would see a diminution of the total amounts invested but still a high level of engagement from investors and agrifood corporations. This means that all things being equal, the speed of transformation of the food value chain will be preserved and even increased. There was never such a good time to be an ag/food/retail entrepreneur or to be a beacon of change inside an established food corporation!