So, it’s that time of the year. Things are moving slower, and we have time to reflect on the past twelve months. Let’s be honest: this has been a challenging year for most of the innovation ecosystems. So, should we forget this year and hope for something better in 2024? Here are four things to remember about 2023:

1 – Investments kept declining, and an increasing number of well-known startups are going bankrupt

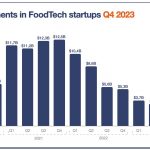

Let’s start with the elephant in the room: while global funding is still significant for FoodTech startups at around $3B per quarter (see our last data on investments). This is a 50% decrease compared to 2020 (and a 75% decrease compared to 2021).

In the meantime, for the first time, the number of FoodTech unicorns is declining with a worrisome number of downturns, low-cost acquisitions, and bankruptcies.

For 2024, we expect a bounce back somewhere between Q2 and Q4. This doesn’t come from our crystal ball but rather from a cold analysis of the historically high amount of dry powder in private equity (a part of which will find its way into venture capital) and the predicted evolution of the interest rates which will make risky investments in startups more rewarding.

2 – The reality check was fatal to many startups and categories

Many startups, and even whole ecosystems, once acclaimed, have been significantly shaken in 2023:

Plant-based: in last year’s “summary” of the year, we said that “people discovered that plant-based products taste bad”. They were not proven wrong this year, and sales kept declining or stagnating in most markets. As inflation slows and consolidation happens, we expect things to get better for plant-based companies.

Vertical farming: many of the major startups operating farms have ceased operations this year. There is hope for this ecosystem’s tech-focused, B2B-minded startups, but they won’t reach the scale and impact of the startups that have disappeared.

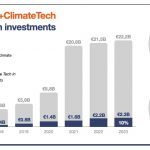

3 – Investments are still running high in some key categories, notably in sustainability and B2B

Investments are decreasing for FoodTech startups. However, the story is not similar for all startups. Some categories are doing surprisingly well, notably:

- Future companies: young, emerging startups are doing quite well and have little difficulty raising funds (compared to previous years). It is much harder for unprofitable, series A+ startups without “hard” assets (defendable tech, strong brand…).

- Sustainability and B2B-oriented startups: even in 2023, very large deals in these ventures are still happening. We even analyse signs of over-hype in alternative protein and decarbonisation (I often wonder if there aren’t more carbon accounting startups than carbon credits emitted and acquired).

- European startups: Europe now weighs 30% of the global FoodTech ecosystem. While it is a bigger slice of a smaller cake, it still shows that something is happening there and that investors (and large companies) are finally noticing it.

4 – Many categories and technologies silently progressed

As I said earlier, innovation slew in 2023, which also affects incremental innovations in established food companies. However, and that’s one of the highs of this year, they didn’t stop their long-term plans and their involvement in startups.

Beyond all the noise created by startups going bankrupt and new deals made in emerging startups, we have observed significant progress in some key points, such as:

- Governments and companies are finally acknowledging the link between food and climate. This was shown by the fact that agriculture was meaningfully addressed for the first time at this year’s Cop 28 (for example, major dairy companies committed to reducing their methane emissions).

- Alternative proteins have made huge progress, from plant-based tasting better to precision cellular agriculture products being authorised in the US (with growing production capabilities).

- The link between health and food has been finally taken seriously with the massive success of weight-loss drugs such as Ozempic.

On a more personal note, I want to thank all our clients. Even in this complicated ecosystem, we witnessed a strong appetite of companies from farm to fork to take the time to think about their place in future of food.