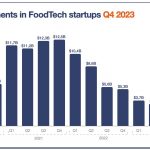

The third trimester is always an interesting period in terms of deals because it is mostly made of one month, September, when startups are announcing all the deals concluded in the past months. When you have deals announced in late July or even in August, you know that we are living in a “boom”. If this was the case in 2021, this summer has been more peaceful, but yet, exciting deals were announced.

Again, as often mentioned in this newsletter, we can’t summarize an ecosystem of thousands of startups to 10 super deals. However, if we consider (as I do) that investors may have a somehow sheeplike mentality, it is a good indicator of where the wind is blowing (in which startups the deals are made) and of their current mood (how big they are compared to the previous period).

Looking at the top 10 deals in the third quarter of 2022 in Europe, we can see that massive deals still went ahead, even if they are far less massive than last year:

📈 Unlike what we hear daily, we observe no slowdown compared to the first half of this year. It just looks like the top deals made in 2021 without the eccentricity of quick commerce (massive investments in startups delivering groceries in 15 minutes or less). We expect 2022 to be a very good year for the Foodtech ecosystem in Europe and probably a record year for all the categories (here is a definition of FoodTech and its different sub-categories) with the exception of Delivery. And even there, new retailers (startups like Picnic, Crisp, Motatos, Oda, Rholik… ) are raising impressive amounts for models that look much more sustainable than quick-commerce.

🇫🇷 +🇬🇧 (🇩🇪 ??) French startups are leading this top 10 ranking, followed by British ventures. That’s a first. To be more accurate, French startups raised more than 50% of all the funds that went into European FoodTech startups in Q3!

Also, we observed no massive deals in German startups, which were leading by far in investments in 2021 (due to quick-commerce notably). Is Germany, and notably Berlin losing its (FoodTech) mojo?

🚜 In terms of topics, the evolution is striking year over year. In Q3, half of the investments went to AgTech startups (notably due to the massive InnovaFeed deal) and 25% to Foodscience. Again delivery startups raised much less than they used to.

And now, what’s next?

🔮 Beyond big deals, looking at smaller deals, we observed that 4 topics are emerging fast: digital solutions for restaurants, anti-food waste solutions (all over the supply chain), carbon credit and carbon counting platforms and alternative proteins.

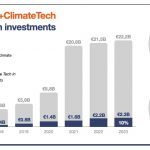

As we explained recently, for us at DigitalFoodLab, FoodTech is not about startups, it’s about the future that our food system needs to become more sustainable (for us humans and the planet). In the short term, some areas will be disrupted, but in the long term, I remain strongly optimistic, especially for Europe, which has all the elements of success.

If raising funds is getting harder, notably from VCs, I do think that there is still no better time than right now for entrepreneurs to launch a new FoodTech venture. Similarly, for food corporations, it is the best timing to plan for the future by investigating, supporting and investing (at a discount) in the ecosystem!